Introduction

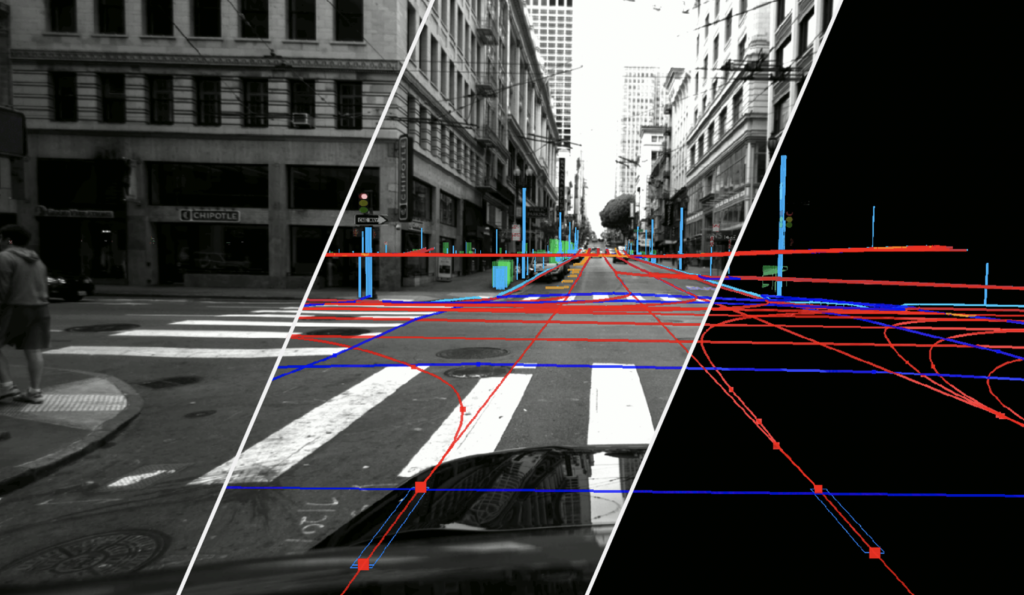

The HD Maps Market is at the forefront of technological innovation, particularly in the realm of autonomous driving and advanced mobility solutions. High-definition maps, or HD maps, represent a sophisticated evolution of traditional digital mapping. These maps provide a high-precision, three-dimensional depiction of the physical environment, meticulously crafted from sources such as aerial imagery, LiDAR data, and GPS inputs. Unlike conventional maps, HD maps deliver centimeter-level accuracy, capturing intricate details like lane markings, traffic signs, curbs, and other road features. This level of detail is indispensable for enabling vehicles to navigate complex urban landscapes with enhanced safety and reliability.

As the automotive industry accelerates toward full autonomy, HD maps serve as the backbone for perception systems in both autonomous vehicles and advanced driver-assistance systems (ADAS). They augment sensor data by offering pre-mapped environmental intelligence, allowing vehicles to anticipate obstacles, adhere to traffic rules, and optimize routes in real-time. The market's significance cannot be overstated: it underpins the transition from human-driven to software-defined mobility, promising to revolutionize transportation efficiency and reduce accident rates through precise localization and path planning.

In 2023, the HD Maps Market achieved a valuation of USD 7.4 billion, reflecting robust initial adoption across key sectors. Looking ahead, projections indicate explosive growth, with the market expected to surge to USD 50.9 billion by 2030. This trajectory is powered by a compound annual growth rate (CAGR) of 31.8% over the forecast period from 2024 to 2030. Such figures underscore the market's potential to become a multi-billion-dollar cornerstone of the global automotive and logistics ecosystems. This article delves into the drivers fueling this expansion, the competitive dynamics shaping the landscape, and the strategic opportunities that lie ahead, all drawn from comprehensive market analysis.

Market Growth Projections: A Decade of Acceleration

The forecast period from 2024 to 2030 positions the HD Maps Market for unprecedented scaling, building on a solid 2023 base year valuation of USD 7.4 billion. By 2030, the market is anticipated to balloon to USD 50.9 billion, driven by the integration of HD mapping technologies into an ever-widening array of applications. This growth rate of 31.8% CAGR is not merely speculative; it is anchored in tangible trends such as the proliferation of electric and autonomous vehicles, where HD maps are non-negotiable for safe operation.

Quantitative analysis reveals that the market's expansion will be uneven but profoundly impactful. For instance, the automotive sector alone is poised to contribute significantly, as manufacturers embed HD maps into production models. The base year of 2023 serves as a benchmark, capturing the market's maturity post the initial surge in ADAS adoption during the early 2020s. From 2024 onward, annual increments are expected to compound rapidly, with revenue streams diversifying beyond core automotive uses into logistics, drone operations, and IoT-enabled services.

This projection is supported by trend analysis methodologies, including value chain evaluations and Porter's Five Forces assessments, which highlight the market's resilience against economic fluctuations. The billion-dollar scale (in USD) of estimations ensures precision in forecasting, covering 28 countries and profiling 15 leading companies. Market share data for 10 of these entities further illustrates concentration among innovators, where early movers are capturing disproportionate value through proprietary mapping platforms.

Key Drivers: Catalysts for Market Momentum

Several interconnected drivers are propelling the HD Maps Market forward, each amplifying the others in a virtuous cycle of innovation and adoption. Foremost among these is the global surge in autonomous vehicle deployment. In 2022, Tesla alone delivered 1.3 million vehicles equipped with semi-autonomous features, a figure that exemplifies the broader industry's momentum. As regulatory frameworks evolve to permit Level 4 and Level 5 autonomy, HD maps become essential for vehicles to interpret their surroundings without relying solely on real-time sensors, which can falter in adverse conditions like fog or heavy rain.

Complementing this is the escalating demand for navigation applications and ADAS integration. Modern vehicles increasingly incorporate features like adaptive cruise control, lane-keeping assistance, and automatic emergency braking, all of which depend on up-to-date, high-fidelity mapping data. The need for precise information on dynamic elements—such as temporary road closures or construction zones—drives continuous investment in map updates, further embedding HD technologies into standard vehicle architectures.

Advancements in sensor technologies represent another pivotal driver. The proliferation of LiDAR, GPS, and inertial measurement units has lowered barriers to HD map generation. For example, in January 2024, Robosense unveiled its M3 and M2 LiDAR sensors, designed specifically to enhance navigation accuracy in autonomous systems. These sensors enable denser data capture, allowing maps to achieve sub-centimeter resolution over vast areas. Aerial imaging, too, has seen refinements, with drone-based surveys accelerating the mapping process for urban and rural terrains alike.

Vehicle safety enhancements round out the primary drivers. Governments worldwide are mandating ADAS in new vehicles, spurring OEMs to integrate HD maps as a compliance tool. This regulatory push, combined with consumer awareness of safety benefits, is accelerating market penetration. Impact analysis of these drivers reveals a high positive correlation with overall market growth, where each percentage point increase in autonomous vehicle sales correlates with amplified HD map demand.

Restraints and Challenges: Navigating Hurdles

Despite its promising outlook, the HD Maps Market faces notable restraints that could temper short-term growth. High installation costs remain a primary barrier, stemming from the expensive nature of high-resolution sensors and mapping infrastructure. LiDAR units, for instance, can cost tens of thousands per vehicle, while comprehensive mapping campaigns require substantial computational resources. These upfront investments deter smaller players and delay widespread adoption in emerging markets.

Privacy concerns constitute another significant restraint. The granular data collection inherent to HD mapping—encompassing roads, buildings, and even pedestrian patterns—raises ethical questions about surveillance and data security. Stakeholders must balance innovation with compliance to regulations like GDPR in Europe, which impose stringent data handling requirements.

Challenges overlap with these restraints, particularly in maintaining map freshness amid rapid urban changes. The need for frequent updates and maintenance services adds operational complexity, while scalability issues arise in covering diverse global terrains. SWOT analyses underscore these as internal weaknesses, yet they also present avenues for mitigation through cost-optimization strategies and privacy-preserving technologies.

Competitive Landscape and Recent Developments

The competitive arena is vibrant, dominated by 15 profiled companies vying for supremacy through strategic maneuvers. Leaders like DeepMap, Inc., Carmera, Inc., and CivilMaps, Inc. are at the vanguard, leveraging product launches to solidify positions. TomTom N.V.'s November 2022 introduction of the TomTom Maps Platform exemplifies this, offering developers tools for location-based innovations integrated with HD capabilities.

HERE Technologies made waves in November 2022 by embedding HD maps into the BMW 7 Series, enabling hands-free highway driving with real-time localization. Similarly, Nvidia's March 2022 launch of Drive Map targets autonomous vehicle OEMs, providing cloud-based, high-precision updates. The Sanborn Map Company advanced U.S. coverage in August 2022 by mapping 4,250 miles of highways, enhancing national infrastructure datasets.

Recent developments further illustrate dynamism. Toyota's May 2023 collaboration with Komatsu Ltd. focuses on autonomous light vehicles for mining, incorporating HD maps for off-road navigation. Google's July 2022 relaunch of Street View HD maps in India, via partnerships with Genesys and Tech Mahindra, addresses last-mile delivery challenges in densely populated areas.

These initiatives, including Baidu Inc.'s AI-driven mapping and Waymo LLC's sensor fusion, highlight a landscape where alliances and R&D investments are key to dominance. Market share availability for 10 companies reveals a fragmented yet consolidating field, with North American and European firms leading in innovation.

Opportunities: Pathways to Future Dominance

Opportunities abound for market participants, particularly in sensor integration and connectivity advancements. The incorporation of thermal imaging cameras promises to elevate map resolution in low-visibility scenarios, while 5G networks enable low-latency data syncing for over-the-air updates. Collaborations, such as those for urban mobility, are unlocking new revenue streams in smart cities and logistics.

Impact assessments of these opportunities project a multiplier effect on CAGR, potentially exceeding baseline forecasts in high-growth regions. Free customization scopes in reports—up to 80 working hours—allow stakeholders to tailor insights, fostering informed decision-making.

Conclusion

The HD Maps Market's journey from USD 7.4 billion in 2023 to USD 50.9 billion by 2030, at a 31.8% CAGR, encapsulates a transformative era in mobility. Driven by autonomous adoption, sensor evolution, and safety imperatives, yet tempered by costs and privacy, the market offers a fertile ground for innovation. As key players like TomTom, HERE, and Nvidia pioneer advancements, the competitive edge will favor those who navigate challenges adeptly. This growth not only redefines navigation but also paves the way for safer, smarter transportation ecosystems worldwide.

Comments